It’s a recession when your neighbor loses his job; it’s a depression when you lose yours. ~ Harry S. Truman

One does not have to be an economic wizard to predict the next recession in the United States. As I write this, I can assure you that all the signs are there. So it behooves one to be prepared. This could be a bad one, one that will spread to other countries.

Economists agree that economic recessions are significant slowdowns in overall economic activity, slowdowns which can and often do last long enough to cause economic contractions. True recessions are characterized by economic decline across all or most sectors of a nation’s economy. This distinguishes them from “structural” crises which can occur in separate industries. True economic recessions, however, can only be confirmed if they last for a period of two or more consecutive quarters so as to nullify any seasonal effects.

Due to the globalization of modern businesses and trade, a recession in one country can easily cross national borders and strike whole regions or the entire world.

A recession becomes visible through decline of all major macroeconomic indicators: GDP (Gross Domestic Product) growth slows down or goes negative; production, investment spending, household incomes and spending. All of these decline while bankruptcies and unemployment increase. Recessions are therefore painful. But are they inevitable downsides of business cycles, as most economists think? This economist isn’t quite so sure. If they are part of natural business cycles, a recession will, in theory, always follow economic periods of expansion. Those who believe that recessions are inevitable have history to buoy their persuasions. They certainly seem to be right.

A normal business cycle usually consists of four successive phases: expansion, boom, recession and crisis. Each phase is important for transition of a cycle. Not only do different social and economic contradictions gain momentum during a recession and crisis, but recessions also establish a basis for future growth. Over long-term periods, the highs and lows of business cycles form the trend, or average, economic growth rate. But a boom phase does not always precede recessions.

Numerous factors that cause recessions can be divided in two large groups – internal (endogenous) and external (exogenous). Exogenous causes are represented by various factors of a catastrophic nature: wars, revolutions and natural disasters. The economy of agricultural countries may be influenced by climatic changes. Coffee producing countries of Central America, for example, are already experiencing serious economic problems caused by climate change. Neoclassical economists also consider state regulations, labor union acts, business monopolies and technological shocks to be exogenous recession factors. In most cases, external factors explain all the economic crises that occurred prior to The Great Depression in the 1930s. The Great Depression was the longest and deepest recession of the 20th Century. It followed a rapid expansion of the U.S. economy, a boom, and overconfidence by investors in an unregulated stock market. Rich people who wanted to be more rich poured too much money into overvalued stocks. And when the market finally crashed, proving the old adage that “what goes up must eventually come down,” millions lost everything they owned. It was triggered by a laissez-faire structural crisis.

Pray that the coming recession, one that will, in my opinion, be triggered by exogenous causes: inept fiscal and trade policies enacted by the current administration, won’t bloom into a Second Great Depression. It could.

Historically, economic expansions in the U.S. rarely last longer than 100 months, and we’re already past that length of time. In fact, there have only been two expansion periods that lasted as long as the one that we’re currently in. To match the record 120-month expansion in the 1990s, we’d need to keep the economy growing past January 2019, an occurrence that The Wall Street Journal deems to be “a very tall order.” It might happen, of course; past performance is not always an accurate predictor of the future. But this, in my opinion, could only come to pass baring a geopolitical/economic shock.

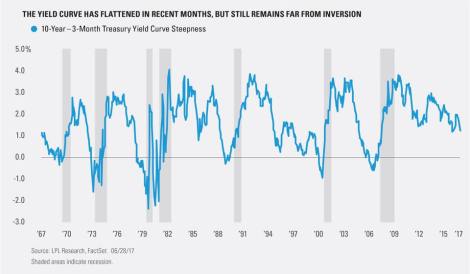

Need I remind you that, thanks to President Donald Trump’s import tariffs, we’re already in the early stages of a trade war with our biggest trading partners: China, Canada, Mexico, and Germany/the EU? In addition, the ten-year/three-month Treasury yield spread, widely used to predict recessions, is nearing inversion. It was all the way down to 0.90 as of June 27, 2018 (the graph shown above is a year old. See what it is today). Recessions always follow spread inversions and, with all the borrowing that the Treasury Department has announced to compensate for lost revenues owing to the recent tax cut, I look for the spread to be in negative territory by July. Therefore, I predict the next recession will occur before the end of the year, probably before the mid-term elections.

Sorry Republicans. It couldn’t happen at a worse time for y’all. But you’ve made your bed… again.

Please feel free to post a comment, pro or con, in response to this article.

Leave a comment